1. Intro: Pay Taxes, or Use For Down Payment?

If you’re a W-2 earner or business owner, you’re paying income taxes every day of your life.

But, if you learn how to leverage real estate strategies to create “paper losses”, you can reduce and even eliminate your taxes every year.

So I ask you:

Would you rather pay $50K+ in taxes every year?

Or use that money as down payment to buy a new property every year?

The IRS gives everyone the choice.

The goal with this Masterclass is to help you understand how to minimize or eliminate your taxes legally, by leveraging the REPS (Real Estate Professional Status) or the STR Loophole (Short-Term Rental Loophole).

Note: Real Estate Professional Status (REPS) is not a real estate license. You don’t need any certifications or credentials to claim it. REPS is simply a tax designation under IRC Sec. 469(c)(7) that allows qualified taxpayers to treat their rental losses as non-passive.

Before diving deeper, let’s clarify why most people can’t automatically use real estate losses to offset their W-2 or business income.

The IRS separates income into two categories:

- Active income — like wages, business profits, or self-employment income.

- Passive income — like rental income or depreciation losses from real estate.

Under normal rules, passive losses can only offset passive income, not active income.

That’s why most high-income earners can’t deduct their losses against their salary or business profits.

However, if you leverage the REPS or the STR Loophole, you unlock one of the most powerful tax advantages in the U.S. tax code: Your real estate losses become “non-passive,” allowing them to offset your W-2 or business income.

That means you can:

- Use bonus depreciation and cost segregation to create paper losses.

- Use those losses to reduce or even eliminate your income tax bill.

- Keep more of what you earn — legally.

Example:

If you earn $250,000 in W-2 income and purchase a $500,000 rental property with 20% down, a cost segregation study could create roughly $150,000 in paper losses.

Those paper losses of $150,000 can reduce your taxable income from $250,000 that you earn, to $100,000.

This reduction of income will put you in a lower tax bracket, and will potentially save you $30,000–$40,000+ in taxes, depending on your tax bracket and filing status.

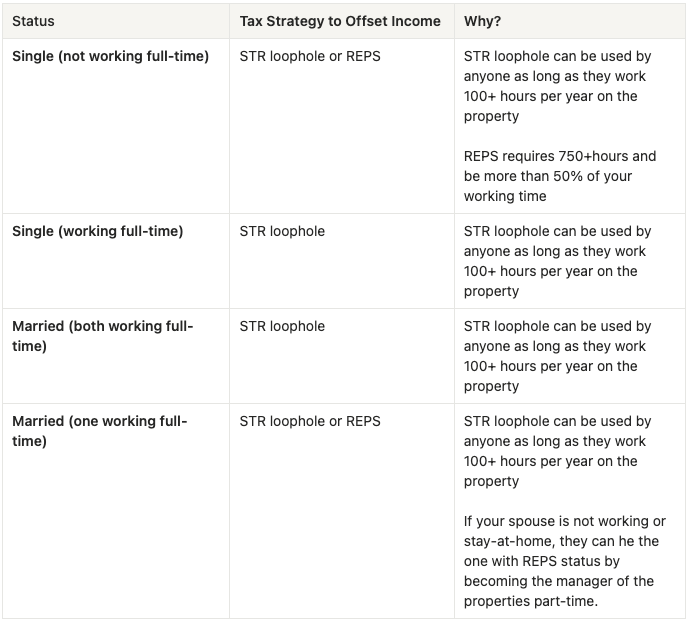

2. What Is Real Estate Professional Status (REPS) and How to Qualify

REPS is a special IRS classification that allows you to treat rental activities as active, not passive.

To qualify, you (or your spouse, if filing jointly) must meet two main requirements:

- More than 750 hours of real estate-related work per year.

- More than half of your total working hours must be in real estate activities.

That means if you work a full-time W-2 job, you personally can’t qualify.

But if you’re married and your spouse has a part-time job or stays at home, she can be the one with REPS on behalf of both of you.

While you’re raking in cash as a W-2 or in your business, your spouse can stay at home, be with the kids, and manage your family’s real estate properties.

Common qualifying activities include:

- Analyzing and buying properties

- Building or remodeling properties

- Finding and screening tenants

- Managing properties

- Visiting properties

- Negotiating leases

- Supervising repairs or renovations

- Bookkeeping and record-keeping

- Attending real estate trainings or networking events

3. What Is the Short-Term Rental (STR) Loophole and How to Qualify

The Short-Term Rental Loophole lets you get REPS-level tax benefits without meeting REPS requirements.

Here’s how it works:

If your property qualifies as a Short-Term Rental (STR) — defined as an average guest stay of 7 days or less — it’s not considered a “rental activity” by the IRS.

That means you can use your STR losses to offset W2 or business income, even if you have a full-time W-2 job.

To qualify, you must:

- Actively manage the property (material participation)

- Meet one of the material participation tests, such as:

- Work 100+ hours on each property per year and no one else does more than you, or

- Working 500+ hours on all properties (if you have several) during the year)

Compared to REPS, you don’t need 750 hours total.

You only need enough time to show that you are actively manage the property.

You can still have a team helping, like a property manager, as long as you work 100 hrs per year on the property and no one else works more hours than you.

Sounds complex, but its pretty easy and easily doable. We can help you with specifics on this.

4. Is REPS or STR Loophole Better for You?

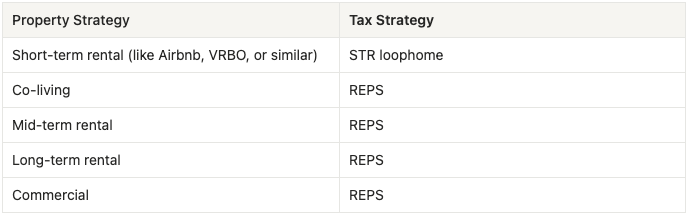

If you only want to own long-term rentals, you’ll need to qualify for REPS to use losses against your income.

Example:

Sarah is a nurse making $200k. Her husband manages their 3 LTRs full-time. He qualifies for REPS, and their $90k in paper losses reduce their taxable income to $110k.

If you only own short-term rentals, you’ll need to qualify for STR Loophole to use losses against your income.

Example:

Jason is an engineer earning $180k. He self-manages an Airbnb, spends 120 hours running it, and no one else works more than he does. His $50k paper loss wipes out $50k of W2 income.

If you own both STR and LTR properties, you’ll need to qualify for REPS to use losses against your income.

5. Properties You Can Use by Strategy

6. Spouses Are the Key to Qualifying for REPS. STR Loophole Works Best for Singles with Full-Time Jobs.

If your family strategy is to have a spouse at home, raising the kids, you MUST take advantage of having the spouse at home be the REPS.

By simply having the spouse at home spend 15-20 hours per week managing the family real estate, the spouse at home qualifies for REPS, and the benefits apply to both on a joint return.

This is why many high-earning couples designate one spouse to manage the properties full-time while the other keeps their W2 income.

The STR loophole, however, is perfect for single investors or household where both spouses want to keep their full-time job.

7. Most Common Tasks That Count Toward REPS or STR Hours

What the IRS wants is for you to be the manager and ultimate decision maker. If you hire a property management company, it will be hard to qualify for REPS.

There is TONS of software (specially AI software) now-a-days that allows you to be the manager in the IRS eyes, but not have to be active daily.

Here are typical activities that count toward your qualifying hours:

- Analyzing and underwriting properties

- Communicating with guests or tenants

- Overseeing maintenance or cleaning

- Managing bookings, pricing, and listings

- Scheduling repairs, walkthroughs, and upgrades

- Reviewing financials or bookkeeping

- Meeting with contractors or agents

- Advertising and marketing the property

- Attending real estate seminars or local REI meetups

8. Day-to-Day Operations in Your Family’s Real Estate Business to Accumulate Hours

Let’s paint a simple, realistic picture.

Daily/Weekly:

- Review tenant messages or guest check-ins

- Schedule cleaners or maintenance

- Analyze new deals on Zillow or Redfin

- Record income and expenses in QuickBooks

- Attend local real estate meetups or webinars

Monthly:

- Review property performance and occupancy

- Visit properties and inspect for repairs

- Update your time log with detailed notes

- File receipts and bookkeeping

- Adjust pricing or marketing based on performance

This consistent involvement helps you build a real, documentable case of material participation — exactly what the IRS looks for.

9. The Infinite “Down Payments Instead of Taxes” Wealth-Building Engine

There’s one thing for sure in this life. For as long as you’re working, you’ll be on the hook for taxes.

If every year your tax bill is $50,000, in 10 years you would have paid $500,000 to Uncle Sam.

But if you put in action the “Infinite “Down Payments Instead of Taxes” Wealth-Building Engine” instead of ending with a $500,000 loss, you will have a $5M gain.

Here’s what we mean:

- Year 1

- Find property #1. Make sure its tax-efficient, self-sufficient, and that cashflows

- Fund the down payment for property #1 ($100,000)

- Put it in service and qualify for REPS or STR Loophole

- Do a cost segregation study to accelerate depreciation

- File your tax return and get a MASSIVE tax return

- Use the tax return from Year 1 to fund the down payment for property #2

- Year 2

- Repeats all over. Infinite loop.

10. Action Plan: When Should You Start?

The answer is today.

Every year you miss this strategy, its costing you roughly 25% of your salary.

You’re working for free for Uncle Sam from January to March.

If you’re busy and would like our help doing this strategy on your behalf, we’d love to help.

Our Real Estate Wealth Management Team would love the opportunity to earn your business.

Click here to schedule a discovery call to see if we’re a fit.